In Ukraine, short-term microloans have become a popular way to handle unexpected expenses. When your salary is delayed, a medical bill shows up out of nowhere, or you just need quick cash to bridge the gap, online lenders step in where traditional banks often hesitate. One of the better-known names in this market has been UkrPozyka. The company promised speed, simplicity, and minimal paperwork, offering money to anyone who could qualify in just a few minutes.

But things have changed. If you’re considering UkrPozyka or just curious about what it offered and why people used it, here’s a full breakdown of its history, features, and the current situation.

What UkrPozyka Offered

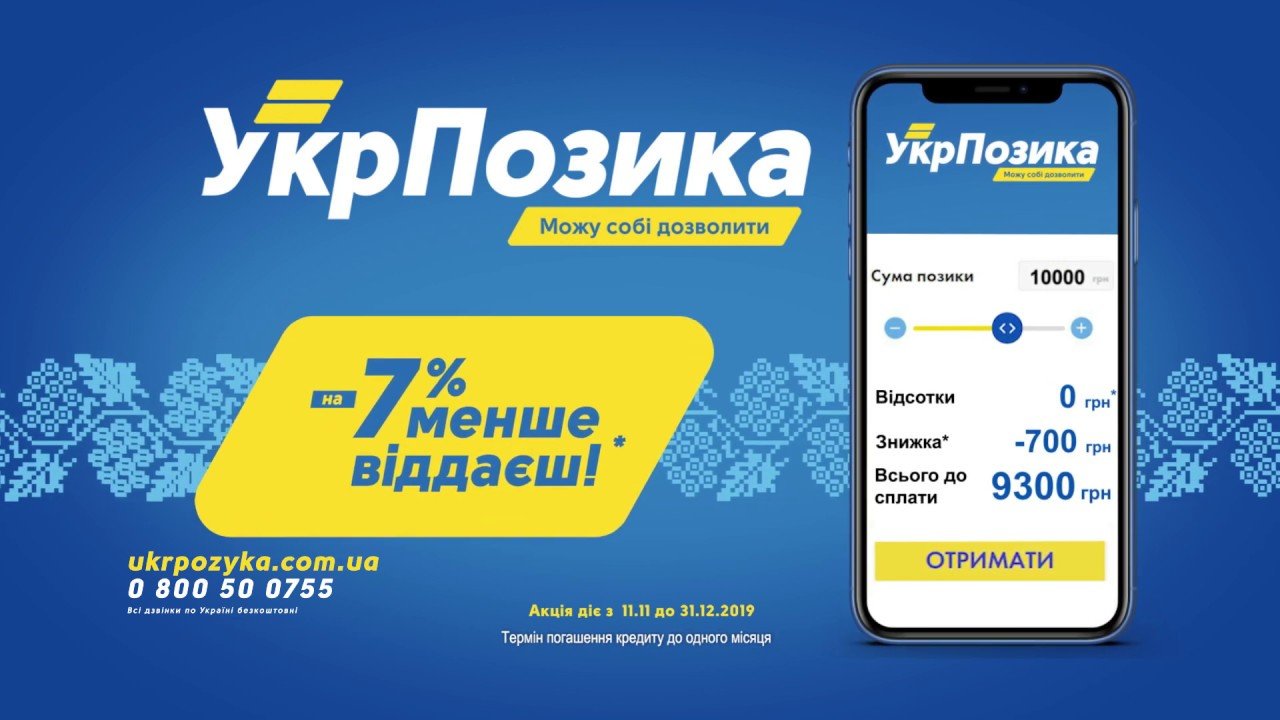

UkrPozyka positioned itself as a fully online microfinance organization. The goal was to make borrowing fast and painless. No need to stand in a bank queue, gather a pile of documents, or wait days for approval. With just a smartphone or computer, Ukrainian citizens could apply and get money transferred straight to their bank cards.

The main selling points were:

- Loan amounts: For first-time borrowers, the limit was usually around 10,000–15,000 UAH. Returning customers in good standing could get more, sometimes up to 20,000 UAH or higher.

- Speed: Applications took only a few minutes, and decisions were often automatic. Many users received funds the same day, sometimes within the hour.

- Simplicity: To apply, borrowers only needed a passport, tax identification number, and an active bank card. No collateral, no guarantors, no long interviews.

- Flexible repayment: Loans could be paid back via the company’s website, through bank transfers, or at payment terminals across Ukraine.

On paper, it looked like a convenient safety net for everyday people who didn’t have access to traditional bank credit.

The Catch: Interest and Penalties

Like most microfinance loans, UkrPozyka’s service wasn’t free money. For new customers, the company often advertised “zero percent” interest on the first loan. But after that, the real cost kicked in. Daily interest rates could quickly make the loan expensive if not paid on time.

If a borrower missed the due date, penalties and additional fees were added. What started as a short-term solution could easily snowball into a much larger debt. Many borrowers praised the speed of the first loan but complained about how quickly costs mounted if repayment was delayed.

Reputation and Customer Experiences

Feedback about UkrPozyka has always been mixed. On the positive side, people liked the speed, accessibility, and the fact that you didn’t need a perfect credit history to get approved. For many, it was a lifesaver when urgent bills arrived.

But there were also plenty of negative experiences:

- Some customers reported aggressive communication from debt collectors.

- Others claimed that payments they made didn’t show up in the system right away, creating stress and confusion.

- Many borrowers felt the real cost of the loan wasn’t clear until they were already locked in.

This balance of convenience and risk is common in the microfinance sector, but it meant UkrPozyka never fully escaped criticism.

Regulatory Problems

The biggest shift came in late 2024, when the National Bank of Ukraine annulled UkrPozyka’s license. Without that license, the company lost its legal right to operate as a registered microfinance lender. In practice, this means UkrPozyka can no longer issue new loans under Ukrainian law.

For potential borrowers, the loss of a license is a red flag. Even if a website or mobile app still functions, customers no longer have the same legal protections. Any agreement made without an active license could leave borrowers exposed, with fewer ways to resolve disputes or challenge unfair practices.

Why This Matters for Borrowers

When people use microfinance companies, they’re often in vulnerable situations—short on money and pressed for time. A licensed lender at least operates under oversight, with certain rules about transparency, data protection, and dispute resolution. Without a license, those protections weaken or disappear.

For Ukrainians, this means that even if UkrPozyka still advertises services, using it could carry serious risks. There are other licensed microfinance organizations in the market that may offer similar conditions but with a stronger safety net.

Alternatives to UkrPozyka

If you’re looking for short-term credit in Ukraine, consider:

- Other licensed microfinance companies that have transparent rates and better customer support.

- Credit cards from banks, which sometimes offer interest-free grace periods.

- Salary advances or employer loan programs, if available.

- Borrowing from family or friends as a last resort.

None of these options are perfect, but each carries different risks and potential costs.

Frequently Asked Questions

1. Is UkrPozyka still working?

No. Its license was revoked, which means it is not officially allowed to operate as a microfinance lender anymore.

2. Can I still apply for a loan with UkrPozyka?

Some websites may still accept applications, but without a valid license, it is not advisable. The risks outweigh the benefits.

3. What were the requirements for borrowing?

Borrowers needed to be Ukrainian citizens, at least 18 years old, with a passport, tax ID, and an active bank card.

4. How much could you borrow?

First-time borrowers could usually get up to 10,000–15,000 UAH. Repeat customers with good repayment history could receive higher limits.

5. What happened if you missed a payment?

Penalties and extra interest were applied daily. This often caused debts to grow quickly.

6. Were there many complaints about UkrPozyka?

Yes. The most common complaints were hidden costs, aggressive debt collection, and problems with payments not registering on time.

7. What should I do if I still owe UkrPozyka money?

Even without a license, outstanding debts may still need to be repaid according to the original agreement. However, you should seek legal advice if you’re unsure of your rights.

Final Thoughts

UkrPozyka once served as a quick fix for cash emergencies in Ukraine. Its promise of fast, simple loans helped thousands of people cover short-term gaps. But the combination of high costs, customer complaints, and ultimately the loss of its license means it’s no longer a safe or reliable option.

If you’re considering a microloan, focus on licensed lenders and read the terms carefully. A loan might seem like a small bridge over a financial problem, but with the wrong provider, it can turn into a much bigger burden.